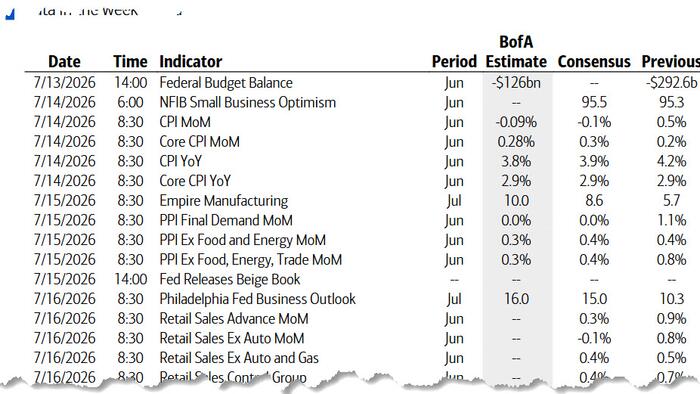

Key Events This Week: CPI, PPI, Retail Sales, Warsh Testifies, China Data, And Earnings Galore

This week presents a critical confluence of macroeconomic data releases and policy signals that will influence broad market direction. The CPI and PPI reports are essential for assessing inflation trajectory and will directly shape Federal Reserve expectations heading into future policy meetings. Concurrent retail sales data provides crucial demand-side validation of economic resilience or weakness.

Warsh's testimony carries particular weight given his position within Fed policy discourse and his influence on market sentiment regarding monetary tightening cycles. His commentary on inflation control and financial conditions will be parsed for forward guidance signals that may trigger sector rotation or risk-asset repricing.

China economic data releases represent global growth implications, affecting multinational earnings expectations and international exposure for large-cap equities. Earnings season acceleration compounds volatility, as investors balance macro headwinds against company-specific performance and guidance revisions. JNJ and other dividend-paying names may face revaluation if rate expectations shift materially.

Sector implication: High-sensitivity sectors including Technology (rate-sensitive valuations) and Financials (net interest margin beneficiaries) will experience pronounced moves. Defensive positioning may be warranted given the binary nature of data outcomes and policy messaging risk.