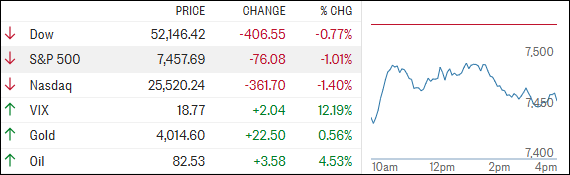

Market weakness extended through the week with the S&P 500 posting losses across multiple sessions, signaling deteriorating risk appetite. The broad index decline reflects institutional repositioning amid conflicting macroeconomic signals and elevated uncertainty, pressuring both growth and defensive positioning simultaneously.

Technology sector underperformance dominated price action, with the Nasdaq absorbing outsized selling pressure. This reflects profit-taking in high-valuation equities and concerns that elevated interest rate expectations may persist longer than previously priced in, directly impacting discount rates for growth-oriented assets.

Geopolitical risk premiums are materializing in broader market dynamics, adding a layer of tail-risk hedging demand. This diversionary pressure typically manifests as sector rotation away from cyclical exposure toward traditional defensive havens, though the data suggests acceleration rather than stabilization in this process.

Sector implication: Technology's acute sensitivity to duration risk and risk-off sentiment is creating divergence within communication services. Streaming platforms like NFLX face compounded headwinds from both sector beta and content spending cyclicality, making them key tactical indicators for broader sentiment inflection.