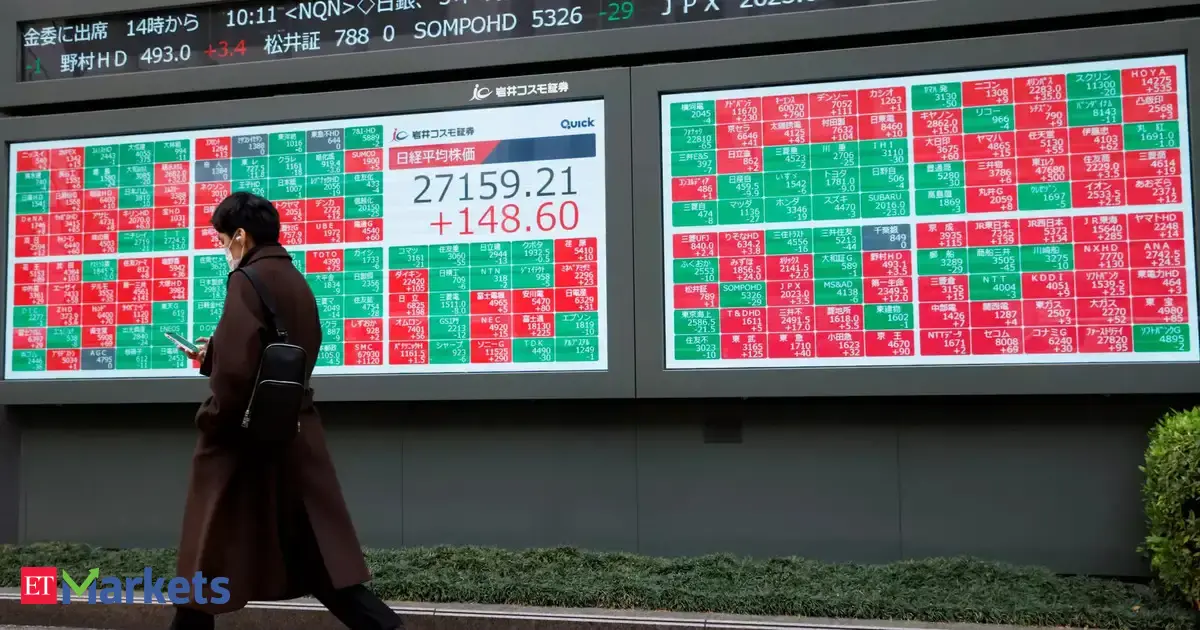

Japan's equity market experienced sectoral rotation dynamics as semiconductor weakness dominated regional tech performance. Kioxia and broader memory-chip exposure declined sharply, reflecting global semiconductor headwinds that extend beyond Japan's domestic cycle. This pullback mirrors international chip selloffs and suggests investor caution on high-valuation semiconductor assets amid macro uncertainty.

The decline in tech stocks triggered classic defensive repositioning. Financial Services and undervalued equity segments attracted capital flows, indicating risk-off sentiment despite the Topix index's recent record-high momentum. This pattern—rotation away from growth into value—often signals intermediate-term consolidation rather than systemic breakdown, particularly in developed Asia.

Toyota Motor and banking shares posted gains, benefiting from both the rotation effect and sector-specific tailwinds. The divergence between semiconductor weakness and auto-industrial strength reflects decoupling narratives: domestic consumption and financing remain resilient even as tech capital expenditure cycles moderate.

Sector implication: The Nikkei's mixed session reflects Asian tech cyclicality intersecting with value-rotation trends. Investors monitoring regional semiconductor exposure should assess whether this reflects temporary profit-taking or structural headwind reassessment in chip demand forecasts.