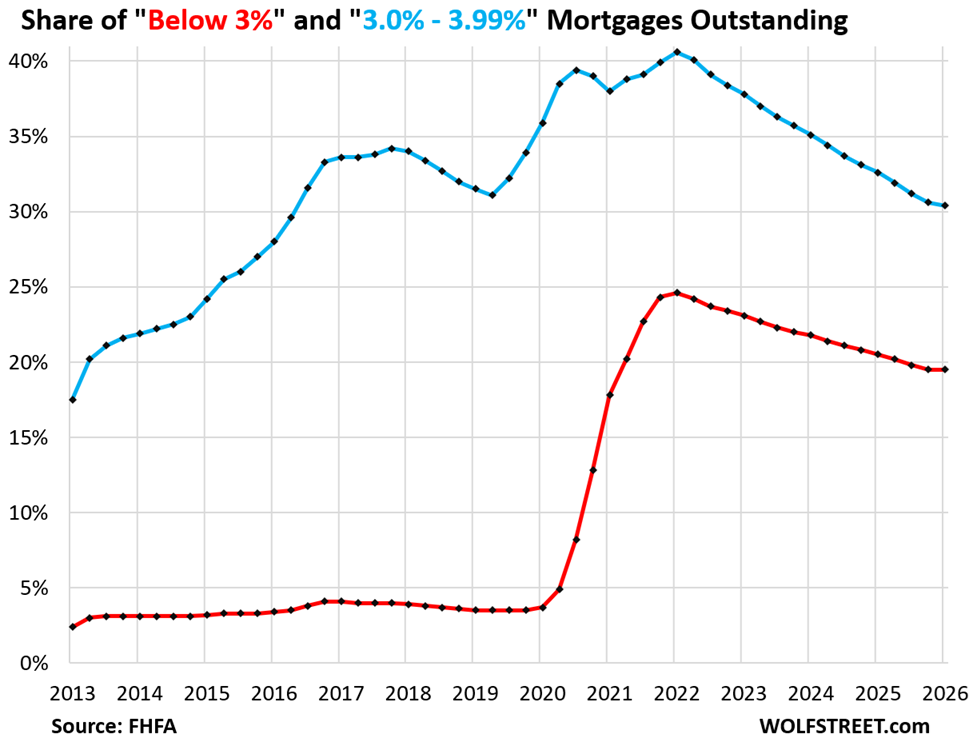

Unwinding the “Lock-in Effect” Suddenly Stalls as Homeowners Stopped Paying Off Below-3% Mortgages

The housing market's structural dysfunction persists as homeowners with ultra-low mortgages (sub-3% rates) have halted early payoff activity, reversing a multi-year trend of accelerated principal reduction. This lock-in effect creates significant friction in the residential real estate market, preventing natural turnover and liquidity that would typically refresh inventory and pricing mechanisms.

Mortgage servicers and government-sponsored enterprises like Fannie Mae (FMCC) face extended duration risk on legacy loan portfolios. When borrowers refuse to refinance or prepay, servicers absorb opportunity cost in a higher-rate environment, compressing net interest margins and yield opportunities. The stalled unwinding suggests refinance-driven portfolio turnover—a key liquidity driver—may remain structurally impaired for an extended period.

This dynamic creates a two-tiered housing ecosystem where price discovery mechanisms remain distorted. Builders compete against a locked-in installed base unwilling to sell, suppressing new construction demand and keeping vacancy dynamics artificially tight. The behavioral freeze suggests rate expectations have shifted; borrowers no longer anticipate rates falling below current levels, eliminating incentive for strategic prepayment.

Sector implication: Financial Services faces headwinds as mortgage origination volumes remain depressed and refinancing pipelines stay dormant. Real Estate pricing power is compromised by this structural stagnation. Expect continued margin compression for mortgage-related businesses and muted housing transaction velocity until either rate expectations reset or economic catalysts force involuntary inventory releases.