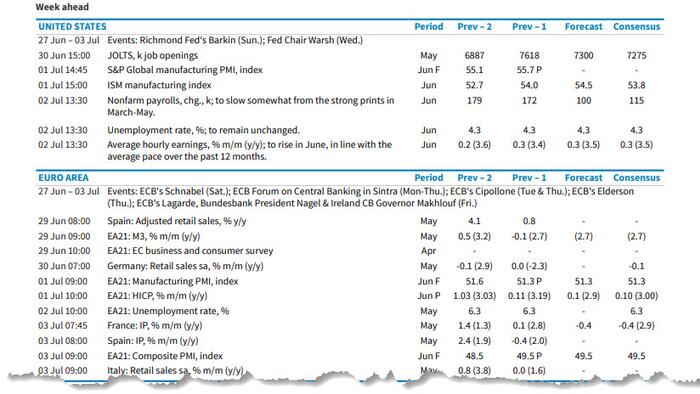

This week presents a holiday-shortened trading calendar with several market-moving economic catalysts scheduled. The convergence of employment data releases, central bank commentary, and manufacturing sentiment surveys creates a high-impact week despite reduced liquidity conditions.

Key focal points include jobs reports (ADP and NFP) alongside ISM manufacturing indices, which will test consensus expectations around labor market resilience and economic momentum heading into year-end. Federal Reserve speaker Warsh at Sintra adds policy-interpretation risk, particularly regarding rate trajectory and financial conditions.

GIS and broader consumer cyclicals remain sensitive to employment data interpretation, as labor market strength directly influences discretionary spending patterns. The shorter trading week amplifies volatility per unit of news flow, increasing execution risk for large institutional repositioning.

Sector implication: Financial Services and Consumer Cyclical sectors face elevated sensitivity to macro data surprises. Equity index futures will track employment metrics closely; any significant deviation from consensus could trigger volatility expansion across duration and equity risk premia, particularly given reduced dealer participation typical in holiday-compressed weeks.