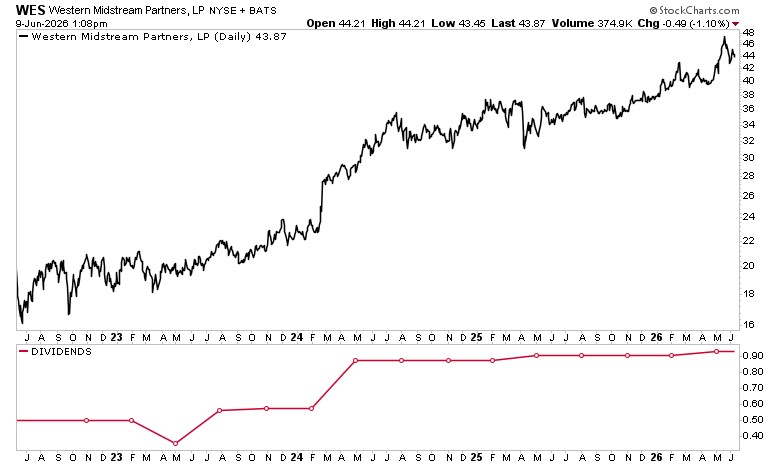

Western Midstream Partners (WES) announced record financial results coupled with a distribution hike, a classic signal of operational strength and cash generation capability within the energy midstream sector. The company's ability to increase payouts while maintaining financial flexibility typically reflects confident management outlook and underlying asset quality in transportation and processing infrastructure.

Midstream operators benefit from volume-throughput and fee-based revenue models that provide stability during commodity cycles. A high-yield distribution increase signals confidence in sustained cash flows, particularly relevant given current energy demand patterns and infrastructure utilization rates. This move positions WES as attractive to yield-seeking institutional and retail investors, potentially supporting capital appreciation alongside distribution income.

The announcement carries modest market-moving weight—it represents company-specific operational execution rather than macro catalyst. However, it reinforces the defensive income narrative within energy, where midstream assets trade on reliability metrics rather than commodity price leverage. Distribution sustainability remains the primary valuation lever.

Sector implication: Positive sentiment for energy infrastructure plays, particularly master limited partnerships (MLPs) focused on fee-based revenue. This supports the broader thesis that energy transition does not eliminate near-term demand for hydrocarbon logistics, strengthening the relative appeal of midstream versus upstream and downstream competitors.