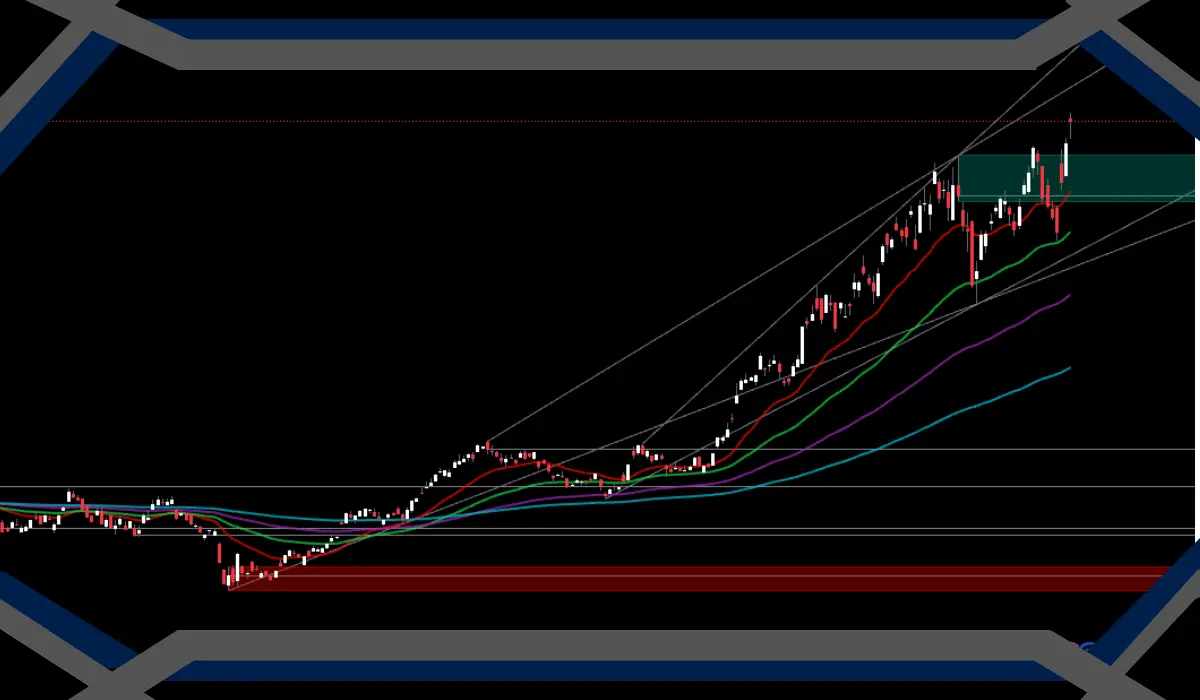

Micron Technology (MU) delivered a 10% single-session rally driven by accelerating artificial intelligence adoption and corresponding memory chip demand. This magnitude of movement qualifies as market-moving, particularly within semiconductor equities where supply-demand dynamics directly influence valuations and forward guidance.

The underlying driver centers on memory capacity constraints across enterprise AI infrastructure buildouts. Data centers deploying large language models and GPU clusters require high-bandwidth memory (HBM) and DRAM at scale, positioning memory manufacturers as critical beneficiaries of the AI capex cycle. NVDA's ecosystem strength indirectly supports MU through correlated demand signals, though Micron faces distinct cyclicality risks.

Investors should calibrate against historical memory chip volatility and competitive pricing pressures. Oversupply risks in 2026-2027 could reverse current euphoria if demand forecasts disappoint. Geopolitical semiconductor restrictions and Chinese competition in NAND/DRAM also present tail risks to extended rallies.

Sector implication: This move reflects renewed conviction in semiconductor exposure within the Technology sector, suggesting rotation away from defensive positioning. However, the magnitude of MU's advance should be contextualized against valuation expansion—if the rally outpaces fundamental earnings revision, consolidation remains probable.