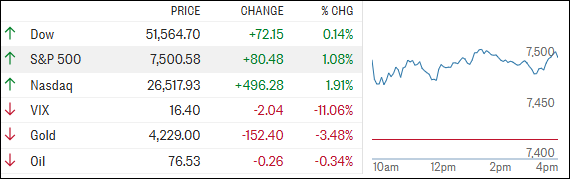

Equity markets demonstrated resilience by reversing prior session losses, driven by a confluence of semiconductor strength and geopolitical developments. The Technology sector led the rebound, with chipmakers NVDA and AAPL capturing outsized gains as investors rotated back into growth equities despite lingering rate uncertainty.

The Federal Reserve's hawkish commentary—signaling potential additional rate hikes remain possible—created near-term volatility but failed to derail the rally. This dynamic reflects a bifurcated market: bond-sensitive equities faced headwinds from tighter monetary policy expectations, yet semiconductor and chip-design leaders outperformed on structural demand and margin narratives independent of immediate rate trajectories.

The Iran MOU announcement introduced a secondary positive catalyst, reducing geopolitical risk premium and supporting energy and cyclical sentiment. Combined with the chip surge, this news flow shifted market psychology from defensive to opportunistic, allowing the S&P 500 to recover ground and break the prior sell-off narrative.

Sector implication: Technology sustained its leadership position despite Fed headwinds, signaling that earnings momentum and secular growth stories are temporarily outweighing macro rate concerns. A sustained chip rally could broaden rally participation if cyclical and financial sectors follow, but Fed policy risk remains the key volatility trigger for subsequent sessions.