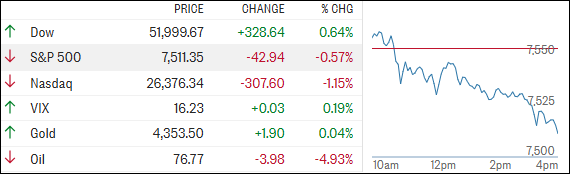

Market breadth today reflects a fundamental tension between momentum-driven rallies and sector-specific headwinds. The Dow's continued strength reflects geopolitical optimism surrounding U.S.–Iran negotiations, which typically benefit large-cap industrials and cyclicals. Conversely, the broad S&P 500 remains range-bound, indicating shallow conviction across the index.

Technology sector weakness amid the session signals potential profit-taking or rotational pressure away from growth equities. This divergence—where large-cap defensive/industrial names outpace tech—suggests investors are recalibrating portfolio positioning toward value and geopolitical-sensitive exposure. The decline in oil prices further pressures energy equities despite dovish macro signals.

SpaceX's post-IPO momentum, while headline-grabbing, remains a micro-cap phenomenon disconnected from broader index behavior. The 10% daily move exemplifies retail exuberance rather than institutional conviction, with limited correlation to systematic market trends. This type of isolated strength often precedes volatility normalization.

Sector implication: The mixed signal—Dow up, Tech down, Oil down—suggests a defensive-rotation trade rather than risk-on acceleration. Institutional flows appear selective, favoring political-sensitivity cyclicals while reducing technology overweight. Monitor whether this represents tactical rebalancing or early-stage sector rotation.