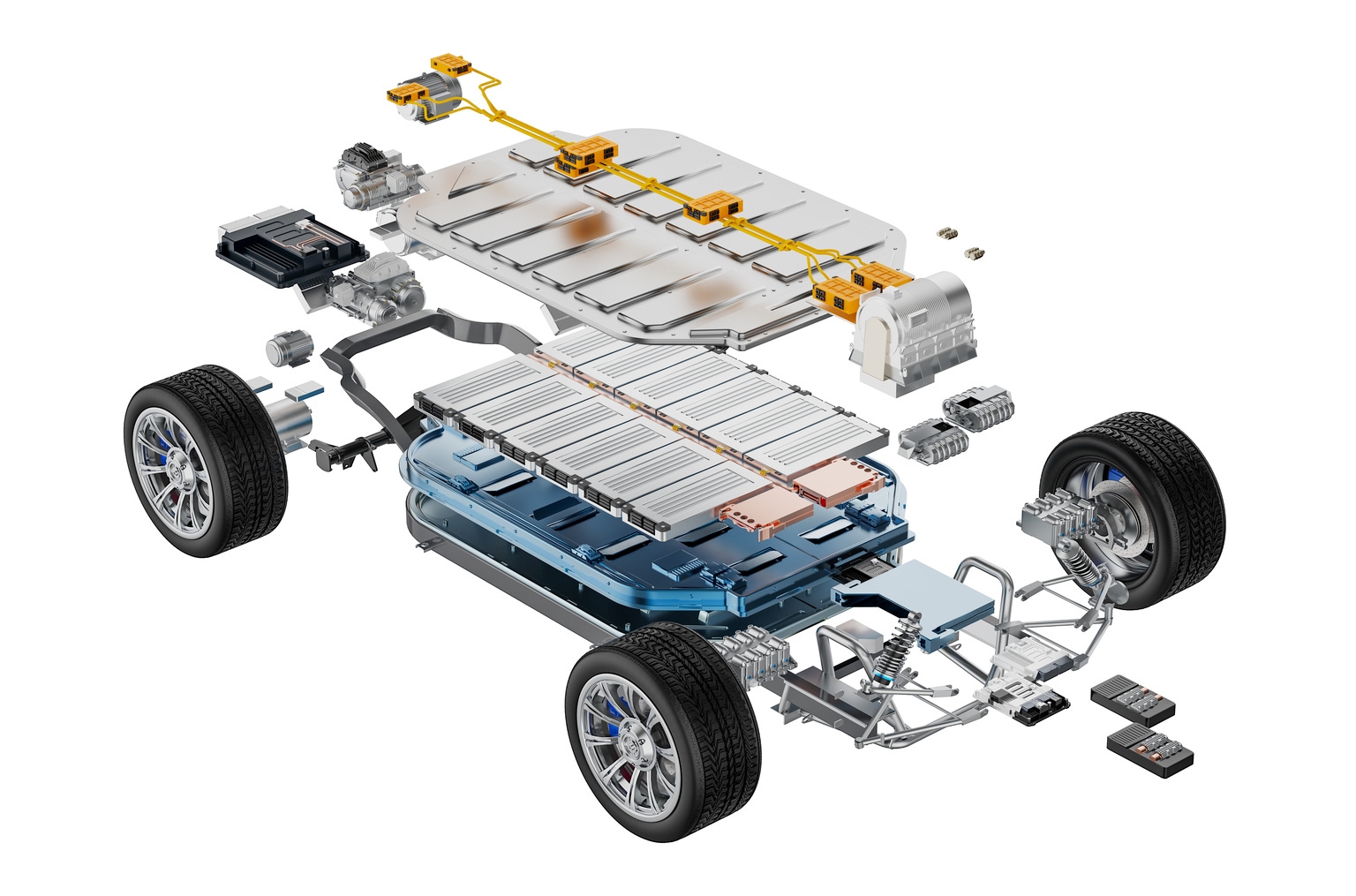

Tesla's competitive advantage in battery technology—historically a core differentiator—is eroding as rivals close the gap in energy density and manufacturing efficiency. This structural shift challenges the company's long-standing moat in the EV sector and raises questions about pricing power and margin sustainability going forward.

The commentary suggests execution risk around TSLA's technology platform roadmap, particularly if development cycles extend or fail to deliver anticipated performance breakthroughs. Simultaneous focus on diversified ventures (SpaceX involvement) may create capital allocation uncertainty and reduce concentration on core automotive innovation, a critical concern for growth-dependent equity valuations.

A narrowing battery advantage could accelerate competitive parity in EV powertrains, potentially compressing Tesla's gross margins and market share assumptions embedded in current forecasts. Investors appear concerned that prior first-mover benefits are being neutralized by scale-up efforts from legacy OEMs and emerging EV specialists.

Sector implication: This thesis underscores weakness in premium growth narratives within Technology and Industrials. A battery-commoditization scenario would favor lower-cost producers and suppliers, reducing single-stock premium multiples. Broader EV and renewable energy plays remain intact, but Tesla-specific concentration risks warrant scrutiny.